Have a question about LifeBright?

Have a question about LifeBright?

Check out our FAQs. If you need further information, feel free to contact investor services and we’ll be happy to answer any questions you have.

Check out our FAQs. If you need further information, feel free to contact investor services and we’ll be happy to answer any questions you have.

Automated Investment Management services are digital platforms that provide automated, algorithm-driven financial planning and investment management services with little to no human supervision. A typical Automated Investment Management service asks questions about your financial situation and future goals through an online survey; it then uses the data to offer advice and automatically invest for you.

Other common designations for Automated Investment Management include “robo-advisors,” “automated investment advisor,” and “digital advice platforms.” Regardless of the name, it all refers to fintech (financial technology) applications for investment management.

The first Automated Investment Management service or “robo-advisor” launched in 2008, with the initial purpose of giving investors that were uneasy about investing a quick and easy way to invest without having to choose their own investments. These services seek to help manage passive, buy-and-hold investments through a simple online interface.

The technology itself was nothing new. Human wealth managers have been using automated portfolio asset allocation software since the early 2000s. But until 2008, they were the only ones who could buy the technology, so clients had to employ a financial advisor to benefit from the innovation.

Today, most robo-advisors use passive indexing strategies optimized using some variant of modern portfolio theory (MPT) Additionally, they can handle much more sophisticated tasks, such as tax-loss harvesting, investment selection, and retirement planning.

One of the big drawbacks of robo-advisors is that they lack empathy, or personal interaction. While most who use robo-advisors tend to need/want less interaction, there are many that like the comfort of having their own advisor that they can call to ask questions. At Lifebright you will have your own advisor you can speak with. You will know their name, and more importantly, they will know yours.

At Lifebright there are never extra fee’s for premium services like tax-loss harvesting, or having your own advisor.

It’s this added benefit that sets Lifebright apart from it’s peers.

At LifeBright, every investor will have a dedicated, credentialed advisor*. If you have a question not included in our FAQs, we are happy to speak with you. (801)500-5038.

You can call customer support to help you with:

If you need deeper personal attention for managing your financial life and meeting your goals, then you may want to consider a traditional wealth manager over an online investment provider. This type of relationship would have a higher fee structure for robust planning and advice.

A credentialed advisor is one that holds an accredited financial planning designation.

A Certified Financial Planner / CFP,

and

Chartered Financial Consultant, ChFC® are among the most recognized.)

Of Course!

We understand that some individuals will just want someone to handle the set-up and management their investment accounts. To open your investment or IRA account just open your investment or IRA account!

Others may just want the financial consulting to help them organize their finances and make sure they are making good financial decisions. To schedule a complimentary consultation regarding financial consulting, or questions with either service, click here for financial consulting!

These two services can be used in conjunction with one another, or as stand alone services.

You’ll finish the process for creating your account with LifeBright within one to two days. As soon as you open and fund your account, we’ll allocate your investments according to your unique profile and investing needs.

The processing time for allocating your funds depends on how you funded your account.

FUNDED WITH CASH FROM YOUR BANK

When you fund your account using cash from a bank account, the funding process will usually take one to two days after you open your account.

FUNDED BY TRANSFERRING MONEY FROM ANOTHER BROKERAGE ACCOUNT

When you fund your account using assets from another brokerage account, the funding process will usually take up to 10 days after you open your account.

You’re always free to log into your account and track the progress of your account opening and funding, as well as any transfers and investments you’ve made.

When you sign up for your account, you also have the option to create an electronic transfer authorization. This authorization allows you to move money to and from your bank account into your LifeBright account.

The process is a secure, convenient way to move your money easily and safely, as you need it. You can also use this authorization to set up an automatic investment plan that moves money from your bank account into your investment account with the frequency that you choose, in the amount that you select. This approach makes automatic investing easy.

Yes, you can. To do so, you need to go through your investment profile questionnaire again and reassess your criteria. If the model comes out the same, and you still want to invest in a different portfolio, then you are free to choose another option. When you make this choice, you’ll sign a disclosure stating that you are asking to invest in options outside of your risk-profile parameters. You do not need to sign this disclosure if you move to a more conservative portfolio or one that is a completely different structure.

Rebalancing portfolios from time to time is helpful in keeping your investments consistent with your selected model, as well as continuing to support tax efficiency. We typically rebalance all portfolios at least at year’s end. This will be an asset-allocation rebalance that also harvests gains and losses in taxable accounts. Some market circumstances may cause us to rebalance more or less frequently, such as:

1. SUBSTANTIAL VOLATILITY

Sometimes, the market experiences substantial volatility. When this environment occurs and causes portfolio allocations to drift too far away from their targets, we’ll rebalance your portfolio to bring it back on course.

2. MINIMAL VOLATILITY

We may choose to not rebalance your portfolio if very little volatility occurred in a given year and your portfolio is still on track with your selected model. We may also choose to not rebalance your allocation if your portfolio is performing as needed in relationship to your risk/return profile.

While we hope to never see a client go, we understand that sometimes this happens. You have complete control over when you close your account.

To close your account, you just need to notify us via email of your desire, and as soon as we receive your request, we stop managing your assets. Once you close your account, you will still own your TD Ameritrade account. You can either choose to liquidate your account or transfer the funds to another brokerage firm. We are always here to help you understand your options and pursue the account-closure solution that best fits your needs.

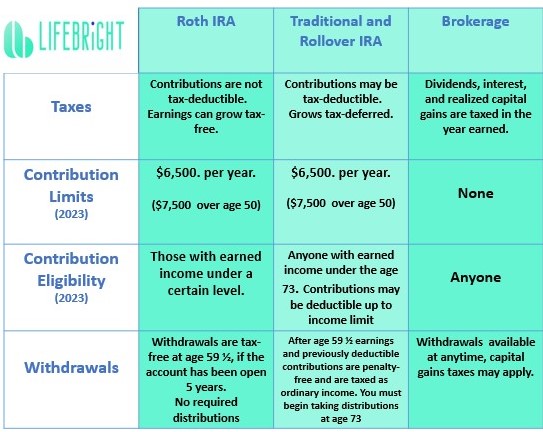

The biggest difference is how and when taxes are paid. Roth IRA’s and regular brokerage accounts are funded with “after tax dollars” meaning you have already paid taxes on the money going in. With a Roth IRA there are maximums per year that you can contribute, and all money (principal and interest) grows tax-free.

A traditional IRA as well as a Rollover IRA invest money “pre-tax”, meaning no tax has been paid on the contributions. There are also annual maximums that you can contribute each year. This could be money that was rolled over from a prior 401(k) plan where money was deducted from your paycheck before it was taxed, or money that you invested in an IRA that you were able to deduct on your tax return, thus lowering your taxable income. With traditional and rollover IRA’s the earnings grow tax-deferred, not tax-free. This means you are “deferring” paying taxes on this money until you begin to use it.

A person would open a Rollover IRA if they were leaving a company and needed a place to move their 401(k) balance.

(This applies to other employer sponsored retirement plans i.e 457, 403(b) 401 (k) etc.)

-Constant financial health monitoring through the Elements Financial Planning app by your Certified Financial Planning, (CFP®) professional.

-Unlimited access to your CFP® via phone, zoom, and email.

-Semi-annual phone/zoom reviews with your CFP®

-Investment analysis and recommendations for your 410(K), IRA, Roth IRA, and standard brokerage accounts.

-Employer Benefits Review

-Insurance Analysis

-Net Worth Analysis

-Investment Tax Planning

-Savings goal planning and progress monitoring

– Debt Management Strategies

-Cash Flow Analysis Strategies

There is a one time initial Financial Assessment/Analysis/plan fee of $299. (Most firms charge $500+). The annual cost for monitoring and ongoing support for planning and consultations is $800.00 per year, paid in advance, or $75.00 per month with a one year agreement)

We accept Visa/Mastercard/Discover as well as debit cards.

There is no cost to cancel once your year commitment has ended. Every year, you will meet with your CFP and evaluate the value that they have provided ,and you have the option to proceed with another year’s worth of service. If you decide not to opt in for another year you are free to cancel at no charge.